Bloomsbury Associates

Bloomsbury blog Taking risk early

Bloomsbury blog post, 23 March 2026

As financial advisers, we sometimes meet clients who need to invest more aggressively than they naturally feel comfortable with to reach their long-term financial goals. When that's the case, it's usually smarter to take extra risk earlier rather than later. Over time, the aim is to gradually reduce risk. As investors move closer to the stage where they stop adding to their portfolio and start withdrawing from it, the order in which returns occur – sequence risk – becomes far more important.

Sequence risk: A bad run at the wrong time

Sequence risk is the danger that the timing of returns harms your plan, even if the long-term average return is the same. A bad run of returns at the wrong time, like just before or after you start withdrawing, can substantially shorten how long your money lasts.

When you start investing, your initial contributions are only a small part of what you'll invest over your lifetime. Poor returns early on hurt less because future contributions are invested at lower prices. However, once you start withdrawing, the same downturn can be much more damaging because you crystallise your losses by selling assets at lower prices.

Sequence risk could help or hurt

To show the impact of sequence risk, we compare two hypothetical portfolios with the same annual returns, but in opposite order. We then look at how these scenarios play out when the investor is accumulating versus when they are withdrawing.

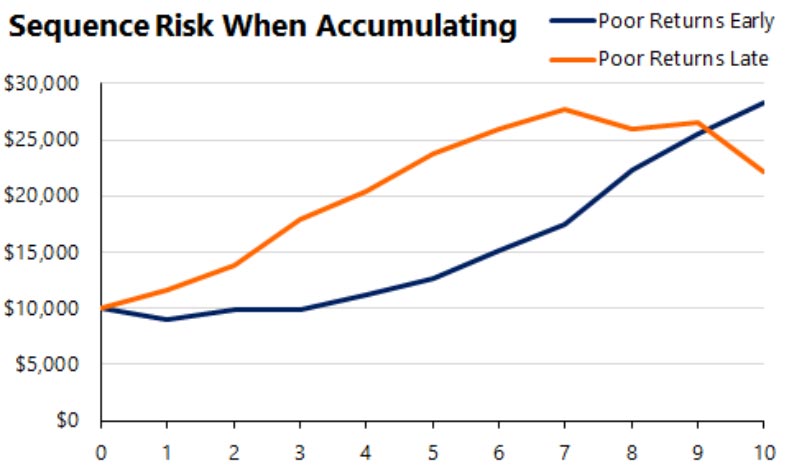

For accumulating investors, we looked at two investors who both start with $10,000 and then add $1,000 at the end of each year. Both receive identical returns over ten years, but in reverse order – one gets poor returns early, the other gets poor returns late.

The results show that poor returns early on aren't necessarily bad for accumulators. The investor who had poor returns at the start ended up with a higher balance after ten years, even though both had the same average return. This is encouraging for those still working and saving – in some cases, downturns can actually help by letting you buy investments at lower prices.

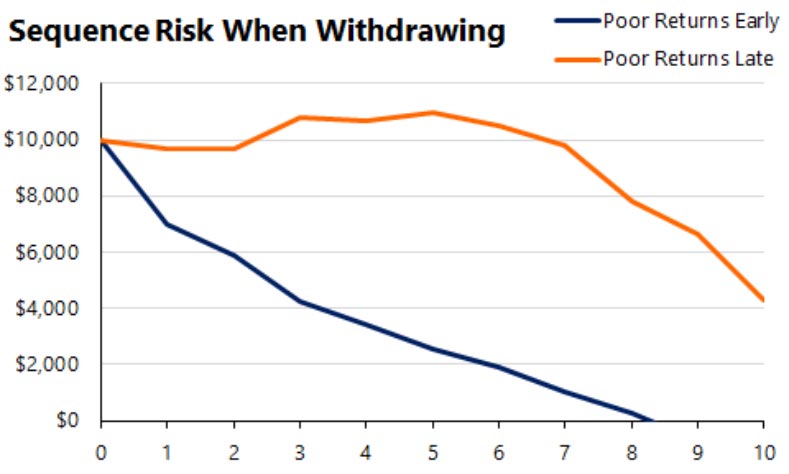

Next, we looked at investors who are withdrawing. Using the same scenario, both withdrew $1,000 each year instead of contributing. Again, one had poor returns early, the other late.

Here the difference was dramatic. The investor with poor returns early ran out of money years before the one who had poor returns later. This shows why investors need to reduce risk once they stop contributing. Lower risk helps protect investors who are withdrawing from significant market downturns.

How can investors manage sequence risk?

If you're still adding to your portfolio and plan to do so for a while, market downturns shouldn't be viewed as a bad thing. Market downturns are an opportunity to purchase investments more cheaply and can boost long-term wealth. Sequence risk is unlikely to affect you until you're close to retirement.

However, if you're about to start withdrawing, or already are, you might need to lower your risk exposure. Protecting yourself from large downturns helps ensure your money lasts longer. Sequence risk is a critical factor that can significantly affect how long your savings support you.

If you want to learn more about how we manage risk for our clients across their investment journey, please reach out to us at info@bloomsbury.co.nz.