Bloomsbury Associates

Bloomsbury blog The problem with performance fees

Bloomsbury blog post, 19 April 2026

There is a fee structure in the investment world that is designed so that most investors never fully appreciate what their investment costs them. It is called the performance fee, and it is one of the primary reasons active fund managers become extraordinarily wealthy – not because of their returns, but because of their fee structure.

What is a performance fee?

There are two common types of fund management fees. The first is a management fee – this is a fixed annual percentage taken from your total assets, regardless of performance. The second is a performance fee, which is a cut of any profits the fund generates above a certain threshold (with the threshold being known as the hurdle rate). The classic (though outdated) structure, made famous by US hedge funds, is the "2 and 20": 2% management fee per year, plus 20% of all gains above the hurdle rate. Performance fees are typically only charged by "active", share-picking fund managers – rather than managers of more passive index-style funds.

Today's funds would typically charge less than the old "2 and 20", more like a "1 and 15", with 1.0-1.5% per year as a management fee and 15% as a performance fee, and a hurdle rate (that returns need to beat to charge the performance fee) of around 7-10% per annum.

We generally have no issue with management fees in principle. Investment managers deserve to be paid for their services and should provide value in some form that the payer desires – a combination of risk management, performance generation and efficiency. While it is perfectly valid to debate the quantum of an acceptable management fee, and to acknowledge that this amount will vary depending on the needs of the recipient, it is generally accepted that the fee should exist at some level. In our view, 1–1.5% is very expensive solely for fund management. We typically exclude funds with management costs that high from client portfolios because the end return on a strategy is unlikely to be the most attractive available.

Performance fees sound reasonable on the surface. Performance fees only "activate" when a manager beats their hurdle rate – so they only profit when you profit. But performance fees do introduce an additional incentive for fund managers – not just to grow your wealth, but to outperform a predefined hurdle. In practice, this can encourage behaviour that's less about stable, long-term wealth growth for investors and more about hitting short-term targets to fuel wealth growth for fund managers.

The real cost of performance fees

To test what these fees actually cost over time, we ran a Monte Carlo simulation modelled on the structure used by Nick Maggiulli at Of Dollars and Data. The simulation runs 10,000 scenarios over 25 years, using the following assumptions:

- The market sees an average annual return of 10% with a standard deviation of 20%.

- The fund charges a 1.05% management fee and a 15% performance fee on returns above a 10% hurdle rate.

- A high-water mark is applied, meaning the fund cannot charge a performance fee in any year unless the portfolio is at an all-time high.

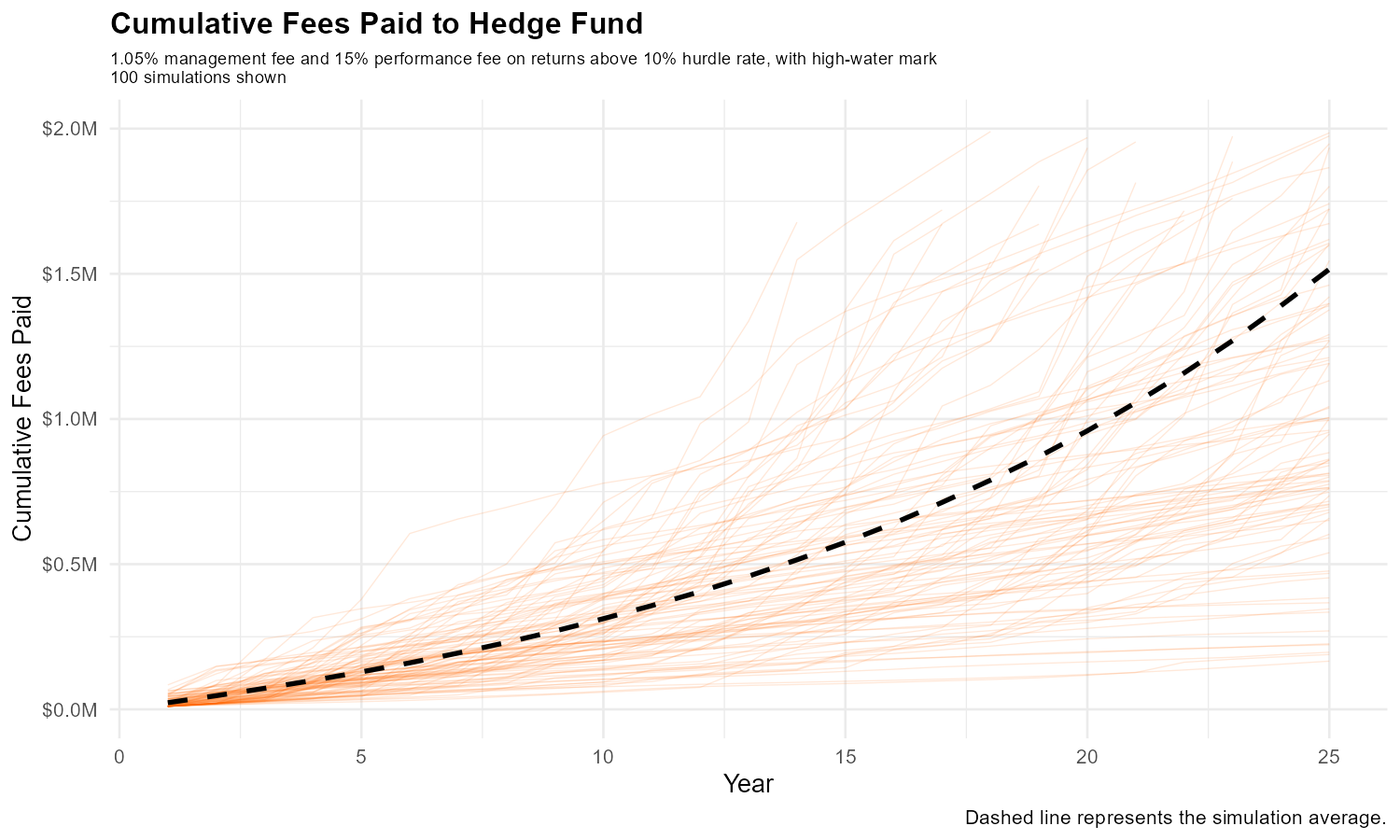

This scenario is based on the actual fee structure of a very popular New Zealand investment fund. The chart below highlights the average cumulative fees over the 25-year period.

Cumulative fees paid to hedge fund

See larger version of this image

After 25 years, the average investor has handed over $1.5M in fees on an initial $1M investment. More revealing is the comparison to an investor who just pays the management fee and doesn't pay a performance fee.

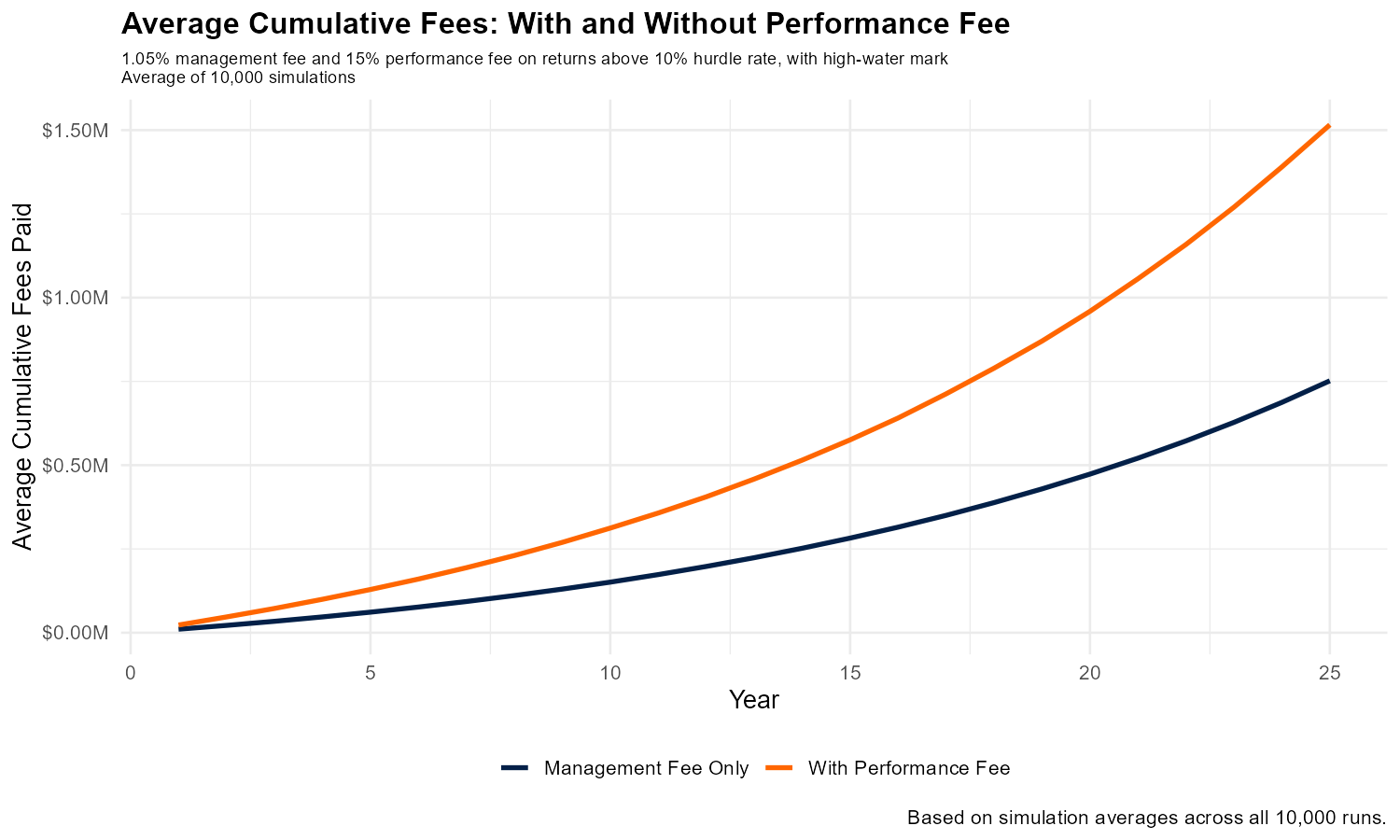

Average cumulative fees: with and without performance fees

See larger version of this image

The average investor paying a performance fee would fork over double the fees of an investor who doesn't pay a performance fee. And this is actually the optimistic scenario for the actively managed fund. The simulation assumes the fund earns the market return – no better, no worse. Let me state that again. For delivering precisely the average return, the investor would be charged twice as much if the fund charged a performance fee for 'outperformance'.

In practice, the majority of actively managed funds underperform their benchmark after fees over long-time horizons. S&P Global's SPIVA research found that only 14.7% of Australian funds outperformed the ASX200 over a 15-year period and in the US only 10.1% of funds outperformed.

Despite the chance of picking a long-term market-beating fund being small, if they beat their hurdle rate in any given year – you pay extra (on top of the exorbitant fund management fee you're already paying).

Some active managers go a step further, structuring hurdle rates in a way that increases the likelihood of performance fees being triggered. For instance, an equities fund with a long-term return expectation of 7-10% per annum may set a hurdle rate as low as 3-5%. Over time, this means you can expect to pay performance fees in many years where the fund has not actually outperformed the broader market but merely beaten an arbitrarily selected hurdle rate.

The asymmetry of performance fees isn't designed for your benefit

Performance fees create an asymmetry that is easy to misunderstand. In good years, the fund takes 15% of your upside above the hurdle. In bad years, you absorb 100% of the loss. The fund never writes you a cheque when markets fall. This is what you signed up for – but it means the risk-reward relationship is fundamentally skewed in the fund manager's favour.

High-quality fund management without performance fees are available to investors now. The industry should throw the terms "performance fee", "hurdle rate", and "high-water mark" away. It's in the interest of investors to stick to one affordable, simple, and consistent management fee.

Performance fees do not make active fund managers rich because they generate above-market returns. They make these managers rich because the fee arrangement is designed for their benefit.

As with any service, a customer or client should receive "value for money". A performance fee is a psychological trick to ensure that the investor overpays for what they receive and that the manager is over-compensated for what they deliver.

Inspired by:

- Of Dollars and Data - How Hedge Funds Get Rich (Hint: It's Not Their Returns)